Will cobots see a post pandemic growth surge?

The market for collaborative robots is forecast to show strong growth over the coming years, with rising sales in industrial and non-industrial sectors and new application scenarios being developed.

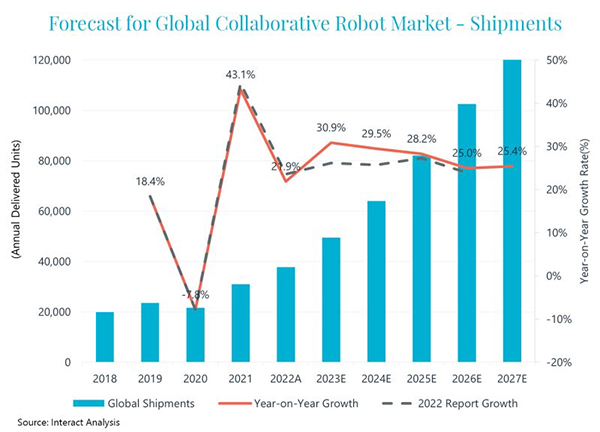

According to Interact Analysis’ newly published ‘Global Collaborative Robot Market – 2023’ report, market revenue grew by 17.2% to US$954m in 2022, with shipments increasing by 21.9% to 37,780 units. Following a rapid rebound in 2021 in the wake of the Covid-19 pandemic, the growth rate of the collaborative robot (cobot) market dropped to around 20%.

The outlook for growth remains optimistic in the medium to long term, with price declines slowing. The compound annual growth rate (CAGR) of global collaborative robot market shipments is anticipated to be 27% over the next five years, with China recording a market CAGR of about 30%, and the South America and Southeast Asia regions both exceeding 30% growth annually. As shown in the graph, the growth rate forecast for the next few years is higher compared with 2022 predictions (grey dashed line).

Unlike the price rebound of traditional industrial robots in 2022, the price of collaborative robots is still declining, but the magnitude of decline is slowing down. The main reasons behind this are:

- In the Chinese market, which accounts for more than half of all shipments, the price decline trend is still significant. Even though most leading component manufacturers have increased their prices more than once, cobot vendors can still control cost within a reasonable range by using local component brands.

- Market competition is becoming increasingly fierce and so it is unsurprising that many leading cobot manufacturers are employing low pricing strategies to drive growth, particularly as they approach a critical juncture for financing or potential listing.

- There have been over a hundred large orders placed in the automotive and non-industrial sectors, driving down average prices.

According to the Interact Analysis predictions, the trend of price declines for collaborative robots will be relatively shallow in the next 5 years. The increase in the proportion of >10kg models combining with the added value of in-machine vision with AI solutions have offset a significant decline in average market prices. As a result, the organisation predicts annual price declines will remain at 3-5%.

Greater intelligence, greater payload

Technologies and solutions related to greater intelligence – including artificial intelligence and machine vision – are increasingly being promoted by collaborative robot manufacturers and are gradually beginning to influence customers’ purchasing decisions. Collaborative robot vendors want to further expand their application scenarios and are looking at ways to increase the perceptive abilities and flexibility of their machines.

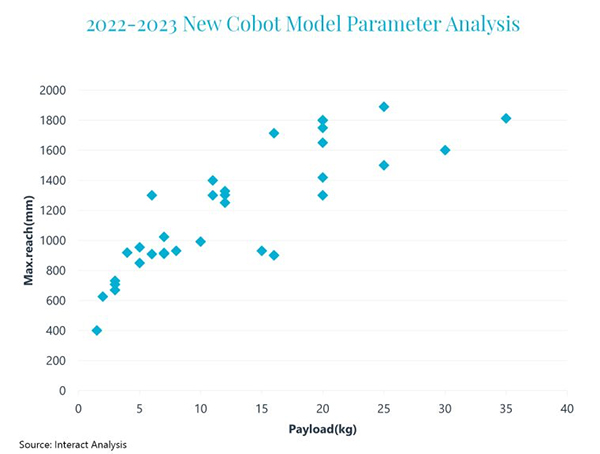

Demand is growing to expand collaborative robot product lines to carry greater payload, partly from the needs of real applications like palletising or welding, and also in order to find incremental market growth space. Faced with inevitable competition from SCARA and high-speed small six-axis robots in the small payload sector, many cobot vendors have begun to take advantage of easy deployment, lightweight body, and high cost-effectiveness to develop models with >10kg payload. The chart presents the payload and arm length of newly launched collaborative robot models from 2022 to 2023, with the growing trend for higher payload and longer arm length clearly visible.

Greater openness, which includes different levels of openness in software and hardware, is also key. Currently, most mainstream collaborative robot manufacturers provide RDKs for system integrators or customers to conduct secondary development. The growing trend towards greater openness will make a more comprehensive range of collaborative robots possible, while also enabling customised solutions to be created more effectively.

Non-industrial vs industrial markets

The global macroeconomic downturn in 2022 struck a significant blow to the non-industrial sector, with the penetration of collaborative robots in industries such as catering, massage, and retail (which are oriented towards individual end consumers) slowing down significantly. The impact of delays to warehousing logistics projects has also resulted in a slower growth rate than expected.

In contrast, as a result of the Covid-19 pandemic, the manufacturing industry has been plagued by work stoppages and labour shortages over the past three years. The demand for upgrading and renovating production lines in traditional manufacturing industries, such as automobiles, metals and general industries, has significantly increased. Coupled with the relocation of factories or production lines by many multinational enterprises in response to supply chain adjustments, and the current trend for reshoring, demand for collaborative robots has significantly increased.

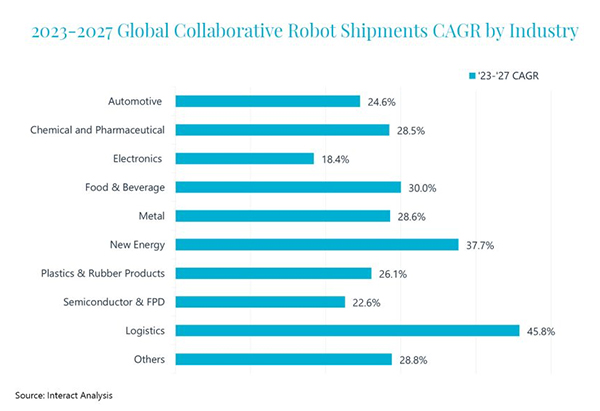

The industry with the fastest growth rate in 2022 was the new energy industry (including lithium-ion battery, wind power, PV and hydrogen), followed by automotive and electronics. This is mainly due to the accelerated growth in various parts of the new energy vehicle supply chain in 2022. Collaborative robots can quickly replace workstations due to their flexibility and ease-of-use.

In addition, collaborative robots have also seen relatively stable growth in industries such food and beverage, and chemicals and pharmaceuticals. Logistics will remain the strongest growth market for cobots, with other industries catching up.

Welding and palletising emerging fast

According to the Industrial Robots report from Interact Analysis, welding and material handling are the two largest applications for industrial robots. In 2022, over half of all global sales of industrial robots came from these two major applications, with the lion’s share coming from heavily loaded articulated robots. In contrast, the proportion of welding industrial robot sales was less than 5% in 2022, but with huge growth potential.

The poor consistency of manual welding and the harsh working environment make welding a key factor in the overall efficiency of a production line, and it is also the most difficult area for many factories to recruit workers. In small factories, flexible and easily deployable collaborative robots can be used to weld small workpieces, while on large assembly lines welding of complex workpieces can also be completed by combining multiple collaborative robots or using a combination of cobots and skilled workers.

Due to the high growth potential of welding scenarios, Interact Analysis has seen major collaborative robot companies, including UR, AUBO, and JAKA, launch specific solutions for welding applications in 2022.